THRIVEFSC

Achieve Financial

Freedom with THRIVEFSC

Tired of minimum payments and high interest?

Apply for our Debt Relief Program:

About Thrivefsc

At Thrivefsc, our mission is to help individuals move beyond debt survival and into a thriving financial future. In a crowded and often confusing market, we stand out by using data-driven insights and strict criteria to match consumers with the most reliable and effective credit and debt relief solutions.

We prioritize our customers’ needs above all, providing them with the clarity and confidence to make the best financial decisions. With Thrivefsc, you’re not just managing debt—you’re building a foundation for long-term success.

Our Core Values

Get Help now

Personalized Debt Relief Plans

Receive customized strategies designed to reduce your debt and help you regain control of your finances.

Expert Guidance

Our experienced professionals will work with you to ensure you make informed and confident financial decisions.

Clear, Actionable Steps

We simplify the process, so you know exactly what to do to start your journey toward financial success.

Ongoing Support

Stay on track with continued assistance and resources to help you achieve lasting financial stability.

Click below to get started and speak with a Thrivefsc expert today.

Services/Solutions

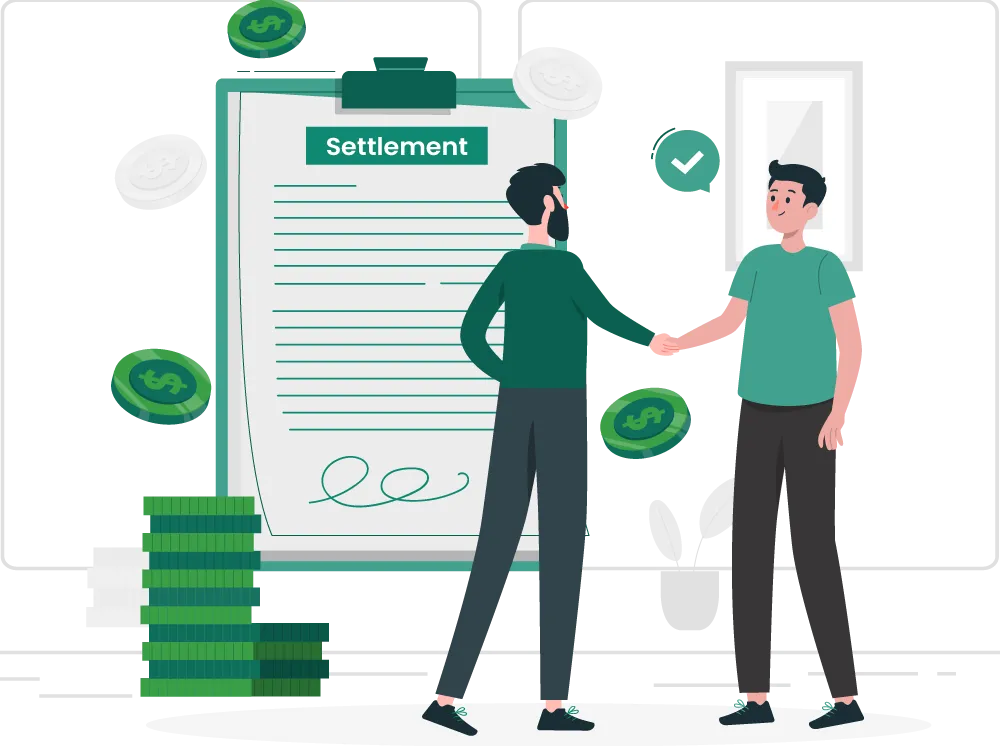

Settlement

What is it?

Debt settlement is a process where you negotiate with creditors to pay off a portion of your debt, typically less than the full amount owed. This negotiation can either be done directly by the debtor or through a debt relief company that specializes in settlements. The goal is to reach an agreement where the creditor agrees to forgive a significant portion of the debt in exchange for a lump sum or structured payment plan.

Debt Invalidation

what is it ?

Debt invalidation is a process where you challenge the validity of a debt, often by disputing errors or inconsistencies in the debt’s documentation. If the creditor cannot provide the necessary proof that the debt is valid and legally enforceable, the debt might be declared invalid, meaning you are no longer obligated to pay it.

Credit Repair

what is it ?

Credit repair is the process of identifying and disputing inaccuracies, errors, or outdated information on your credit report to improve your credit score. This can be done by the individual or through a credit repair company that handles the process on your behalf. The goal is to ensure that your credit report accurately reflects your financial history.

How it Works

Create a profile

Start by providing us with a few key details about your financial situation. This helps us tailor the best debt relief options for you.

See what solutions you qualify for

Our system analyzes your profile and matches you with the most effective debt relief programs. Discover the options that fit your needs.

Create a better financial future

With the right plan in place, take control of your finances and work toward a debt-free future. Thrivefsc helps you build lasting financial success.

Frequently Ask Question

What is the difference between settlement and Invalidation?

Debt Invalidation: This involves challenging the validity of the debt, often through legal means. If successful, the debt is deemed unenforceable, meaning you may not have to pay it at all. This approach focuses on proving that the debt is invalid or that the creditor cannot legally collect it.

Debt Settlement: This is a negotiation process where you agree to pay a portion of the debt in a lump sum, and the creditor accepts this reduced amount as full payment. The remaining balance is forgiven, but the settlement may negatively impact your credit scoreorn

How long will it take to be debt free?

Many of our customers successfully pay off their enrolled debts in just 24-48 months. Instead of spending years making minimum payments and accruing high-interest charges, our debt relief program offers a faster, more affordable, and simpler path to becoming debt-free. Curious about how much time and money you could save? Try our Debt Repayment Calculator today.

Should I keep paying my credit card bills?

Clients join our Debt Resolution Programs because they’re facing challenges in meeting their financial obligations. While we don’t recommend that anyone stop paying their credit card bills, it’s crucial to understand that continuing to make payments may reduce our leverage when negotiating with creditors. Ultimately, the choice to halt payments is yours.

How will debt relief affect my taxes?

Thrive cannot and does not provide tax advice, but generally speaking, if your debt is canceled, forgiven, or discharged for less than the amount owed, the forgiven amount may be considered taxable.

Typically, if the forgiven debt exceeds $600.00, you are required to report it on your tax return for the year in which the cancellation occurred. However, this doesn’t necessarily mean you owe taxes on the forgiven portion. Many clients can legally exclude resolved debt from their income by using the ‘insolvency exclusion’ provided by IRS regulations. This exclusion applies when your liabilities exceed the fair market value of your assets, meaning you ‘owe’ more than you ‘own.’ For more information, please consult the IRS or a qualified tax professional.

Is Debt Relief Right for me?

Like any approach to managing overwhelming debt, the debt relief process has its pros and cons—but only you can decide if it’s the right path for you. Because debt relief requires a significant commitment, it’s important to take some time to reflect on your financial goals by asking yourself a few key questions.

What am I using my credit for? Do my goals require a strong credit score in the short term, or am I focused on achieving an excellent score in the long term? Can I afford to make a monthly payment toward my debts?

Ultimately, you know your situation and financial goals better than anyone. You may decide that debt resolution isn’t the best fit for you, or you may discover it’s exactly what your finances need. If you’re unsure, our team of certified debt specialists is here to help you make an informed decision.